Credit affects almost everything in your financial life — from getting a car to renting an apartment — but most people never learn how it actually works. This guide gives you a clear, no-nonsense look at what credit is, why it matters, and how it impacts your everyday decisions.

1. A Simple Definition of Credit

At its core, credit is the ability to borrow money now and pay it back later. When a bank, lender, or company gives you credit, they’re trusting that you’ll repay what you owe.

You use credit more often than you think:

- When you swipe a credit card

- When you take out an auto loan or student loan

- When you open a new cell phone plan

- Even when you get utilities set up at a new apartment

A helpful way to think about it:

Credit = Trust + a Track Record.

The trust comes from how well you’ve repaid others in the past. Your “track record” shows up in your credit report and credit score.

2. How Credit Works in Everyday Life

You might think credit only matters when you’re buying something big. But it influences many everyday situations you probably don’t expect.

Here are real-world examples of how credit shows up in your life:

- Renting an apartment: Landlords often check your credit to decide if you’re reliable.

- Insurance rates: Auto and home insurers may use credit-based scores when setting premiums.

- Utilities: Electricity, water, and internet companies may require a deposit if your credit is low.

- Employment: Some employers check a version of your report (with your permission) for certain jobs.

When your credit is strong, everything becomes easier and cheaper. When it’s not, you may still get approved — but you’ll likely pay more.

3. Why Credit Matters

Credit impacts two big parts of your financial life:

1. Your ability to get approved

Good credit tells lenders you’re a low-risk borrower. That means you’re more likely to get loans, apartment approvals, or credit cards without hassle.

2. The cost of borrowing

Your credit often determines:

- Your interest rate

- Your fees

- Your loan terms

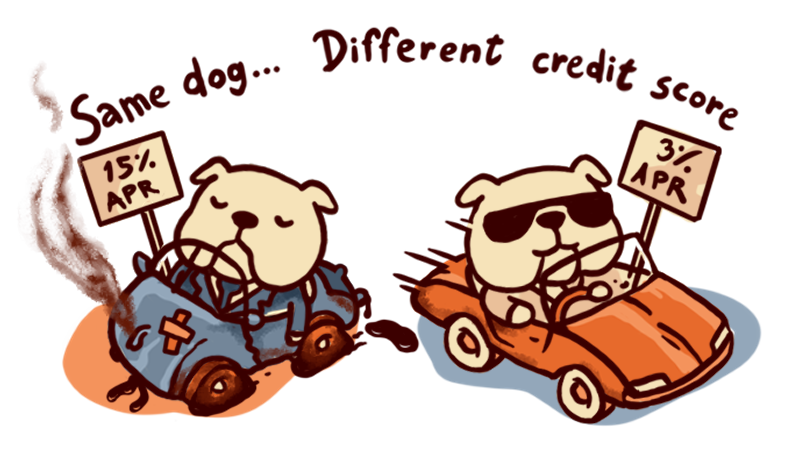

For example, someone with strong credit might pay 3% APR on a car loan, while someone with poor credit might pay 15% APR or more. That difference can add up to thousands of dollars.

To better understand how lenders evaluate your creditworthiness and what your reports actually contain, the Consumer Financial Protection Bureau (CFPB) offers a comprehensive breakdown of credit reports and scores.

4. The Three Pillars of Credit

To understand how credit really works, it helps to break it down into three simple pieces:

1. Borrowing

You borrow money or use a product/service upfront.

2. Repayment

You pay it back on time — or not. Your payment history is the single biggest part of your credit score.

3. Reporting

Your lender sends updates to the credit bureaus, which get added to your credit report.

Every credit decision you make fits somewhere inside this cycle.

5. The Difference Between Credit, Loans, and Debt

These three terms get mixed up all the time, so here’s a simple way to think about them:

- Credit = the ability to borrow

- Loan = a specific type of borrowing product

- Debt = the amount you currently owe

Example:

If you get a $1,000 credit card, the $1,000 limit is credit.

If you spend $400 on it, the $400 becomes debt.

If you take out a car loan, the loan itself is the product, not the debt.

Understanding this helps you stay clear on what you’re managing.

6. Major Types of Credit

There are three main types of credit you’ll see in your financial life:

1. Revolving Credit

You borrow, repay, and borrow again (like a credit card). Your balance changes throughout the month.

2. Installment Credit

You borrow a fixed amount and repay it in set payments. Examples: auto loans, student loans, and mortgages.

3. Open Credit

This is less common. You use the service and pay the full balance each month. Examples: charge cards or some utility accounts.

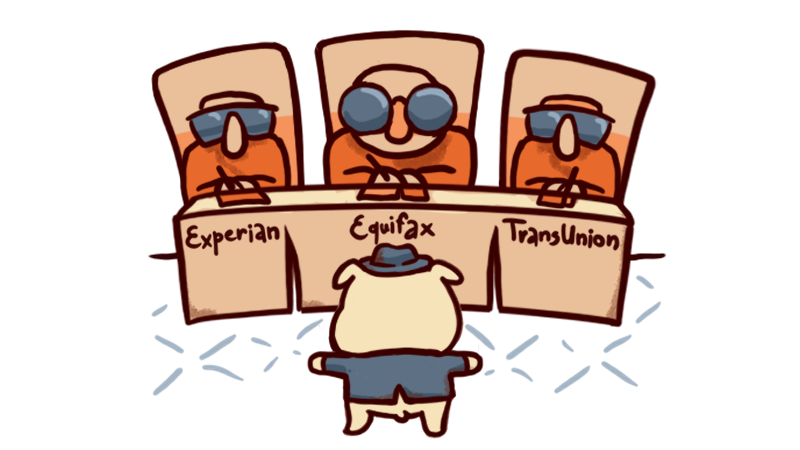

7. Who Decides Your Credit Standing?

Your credit standing (or creditworthiness) is shaped by a few key players:

- Lenders: banks, credit unions, loan companies

- Credit card companies

- Credit bureaus: Equifax, Experian, and TransUnion

- Scoring models: FICO® and VantageScore®

Each group uses your credit report and credit score to decide whether to approve you — and at what cost.

Your official rights around credit reporting are protected by the Fair Credit Reporting Act (FCRA).

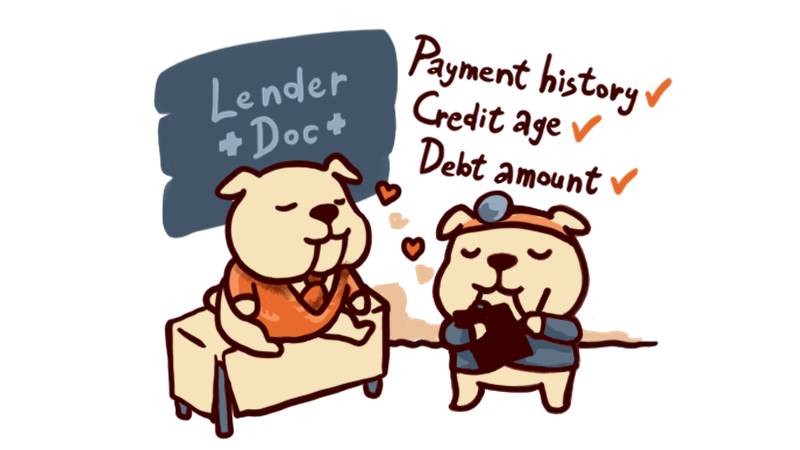

8. What Creditworthiness Means

“Creditworthiness” is a lender’s way of asking:

How risky would it be to lend money to you?

They look at:

- Your history of paying bills

- How much debt you already have

- How long you’ve had credit

- How often you apply for new accounts

- The types of accounts you use

These factors make up most scoring models, including FICO, the most widely used score in lending decisions.

These factors make up most scoring models. If you want a plain-English explanation of what goes into a credit score and how the math works, the CFPB’s guide on credit scores is a clear and reliable starting point.

9. How Credit Is Created (Your First Credit Line)

If you’re new to credit, you may wonder how someone even gets started. Here are the most common first steps:

- Student loans — many people unknowingly build their first credit line through college loans.

- Secured credit cards — you put down a deposit, and the card reports just like any other credit card.

- Authorized user accounts — someone adds you to their existing credit card.

- Credit-builder loans — you pay yourself over time and build credit while you do it.

If you’ve never had credit before, don’t worry — everyone starts somewhere.

10. The Cost of Credit

Credit isn’t free — lenders charge for the risk they take.

Here’s what you pay for when you borrow:

- Interest — the main cost of borrowing

- APR — the total cost of borrowing over a year

- Fees — annual fees, late fees, balance transfer fees, origination fees, etc.

Example:

If you borrow $1,000 at 20% APR, your cost of borrowing is much higher than someone who borrows the same $1,000 at 7% APR.

11. Common Misconceptions About Credit

Let’s clear up some myths that confuse almost everyone:

Myth #1: You need to carry a balance to build credit.

False. You can pay in full every month and still build excellent credit.

Myth #2: Checking your own credit score hurts it.

False. Pulling your own score is a soft inquiry and has zero impact.

Myth #3: Income affects your credit score.

Nope. Income isn’t included in credit scores — although lenders still look at it separately.

Myth #4: Closing old accounts boosts your score.

Usually false. Older accounts help your credit history, so closing them can sometimes hurt.

Final Thoughts

Understanding credit doesn’t have to be complicated. When you know how credit works — and how lenders judge your creditworthiness — you can make smarter decisions that save you money and open new opportunities.